Sharp drop in EU-ETS Emissions could pose a risk to the current rallye in EUAs

The price for EU Emissions Allowances (EUA) dropped sharply by around 40% in the March crash 2020 but has since then recovered above pre-COVID19-levels. On 16.09.2020 The EU comission announced the plan to reduce emissions by 55% instead of 40% by 2030. There is plans to include additional sectors into the EU-ETS and a Carbon Border Tax is also being discussed. More details on these measures are expected in June 2021. On the back of these news the price of EUAs has reached all time highs in 2021.

Although the long-term picture with the political will to reduce emissions looks bullish for EUA prices, the short-term fundamentals (e.g. of 2020 with the COVID19 containment measures) look rather bearish.

With more data on power generation being available I did an update on my old estimation.

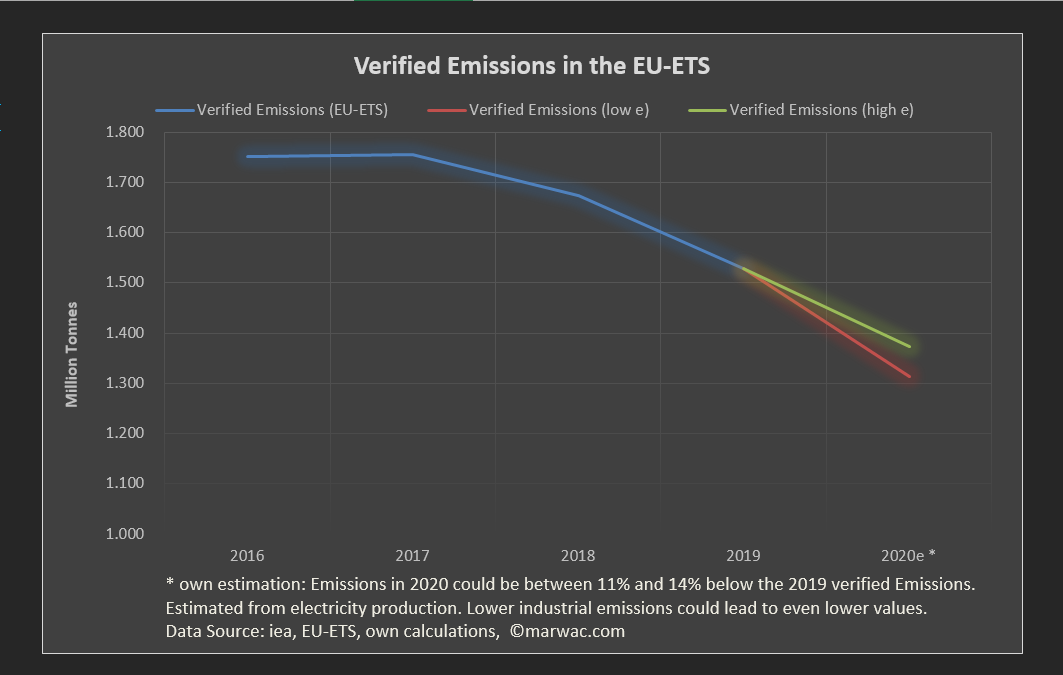

In this analysis I have infered the Verified Emission estimate from electricity production data.

- Verified Emissions (high e) by recovering back to the electricity production and structure from December 2019 in December 2020. Resulting in -11% (-156Mt) Verified Emissions versus 2019.

- Verified Emissions (low e) by continuing in December 2020 with the same electricity production and structure as reported in the first 11 months of 2020. Resulting in -14% (-217 Mt) Verified Emissions versus 2019.

The paths for the two scenarios are shown in the graph below.

The impact on the EU-ETS could be even stronger. Verified Emissions could drop even more than 14% in case the demand for EUAs from industrials is falling stronger than the demand from the power sector.

Furthermore the Airline sector ist still receiving free allocations. In the past they have not been sufficient and airlines have been buying EUAs for compliance. In 2019 emissions in the EU-Airline ETS were 68.24Mt. There was a free allocation of 32.2Mt which means the remaining 36.04Mt needed to be purchased as EUAs from the EU-ETS. Estimations by the IATA in April 2020 expected a decrease of 38% in airline emissions.

On 26th of January EUROCONTROL expects emissions from airlines in the EU to be down by 56.9% versus 2019. This would approximately lead to airline emissions of 29.41MT and therefore be within the free allocation. There should not be any demand from airlines to buy EUAs from the EU-ETS for compliance in 2020. This is additional bad news for EUA demand for the 2020 compliance.

With the expected drop in verified emissions in 2020 the EU-ETS will be oversupplied in the short term and this poses a strong downside risk when compliance data is going to be reported in March 2021.

The new -55% emissions target should lend support for EUA prices in the long run. This support will be watered down if the EU or member states implement further subsidies outside the EU-ETS for CO2-free energy production or other CO2 reductions.

It will be interesting to see if the long term view can hold prices up then.

The opinions expressed here are the personal opinions of the author and also no investment advice.

Links:

https://www.eurocontrol.int/publication/eurocontrol-data-snapshot-co2-emissions-flights-2020

https://ec.europa.eu/clima/policies/ets/allowances/aviation_en

https://ec.europa.eu/transport/sites/transport/files/2019-aviation-environmental-report.pdf